(1.3) Module Narrative

Module 1 Narrative – Start From Where You Are

Module 1 Narrative – Start From Where You Are

Figure 1-1 Start Where You Are

Financial Literacy Check out this link for more info on Financial Literacy!

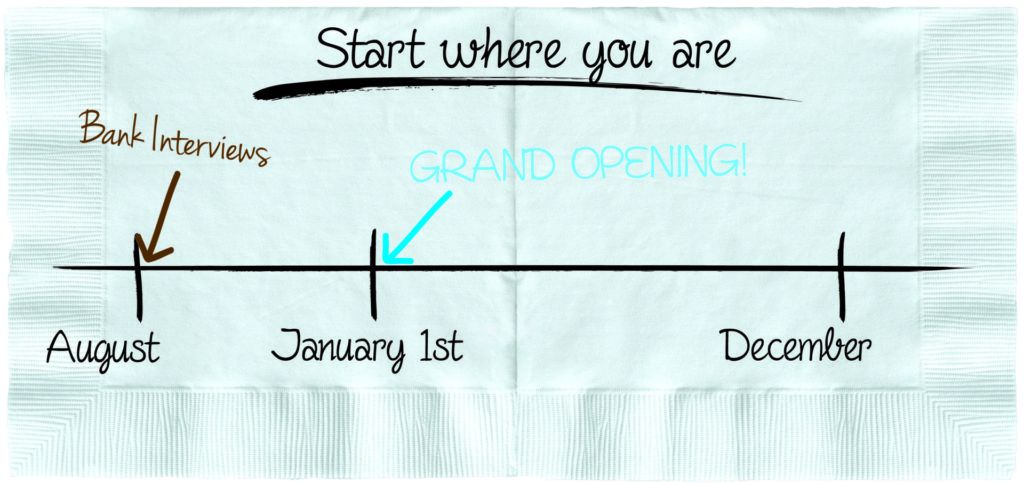

Beth Smith, a faithful part time Corner Bakery employee was offered to take over the ownership of the bakery due to the owner’s terminal health. The owner, Nancy Jackson operated the successful family retail business as a sole proprietorship for more than twenty years. Unfortunately, due to Nancy’s unexpected health condition in August 2025 she was encouraged by her physician to sell or close the business. Beth and her husband, Bob saw the potential of operating the bakery with the family support – two college aged daughters and two sons in high school. Beth and her husband had many discussions concerning business ownership risks and rewards before committing to the Jacksons’.

Both families agreed to set January 1, 2026 as the date for transfer of ownership. This provided five months for Beth to prepare financial planning, marketing and other arrangements to be made. In the months prior to the Corner Bakery opening under Beth’s management she committed time to writing a business plan with the owners’ assistance since Nancy had years of experience.

Financial Risks/Financial Rewards

Entrepreneurship Check out this link for more info on Entrepreneurship!

It was Beth’s idea that they use this opportunity to inform the four children of the risks and rewards of business ownership. Secondly, she thought it provided opportunity to teach them about personal and business finances. Beginning in August 2025, the family planned sessions after evening meals which provided the parents an opportunity to teach the children. Aspiring entrepreneurs must understand that there are no guarantees. None! A new business start-up offers financial risks as well as financial rewards. The parents carefully instructed the children of both.

Business Ownership Rewards:

Small Business Check out this link for more info on Small Businesses!

- Opportunity to increase household income: Additional income will be needed since the two older children were attending the local community college

- Work ethics – the children will be assigned responsibilities

- The children will learn fiscal responsibilities

- The parents will have an opportunity to include family members in the decision making

- The children will be learning risk taking first-hand

- The children will develop financial literacy skills

- Independence: entrepreneur highly value their independence as a small business owner

Business Ownership Risks:

Risk / Reward Check out this link for more info on Risk and Reward!

- The Smith’s will be opening the new business in January 2026 during an economic downturn in the local economy

- Beth and Bob are pledging all their life savings to guaranteed the bank loan

- Beth who is the aspiring entrepreneur has no experience in business ownership

- Beth’s parents’ assets are at risk also since parents co-signed the bank loan

- Banker who loaned the money may ‘call in’ the loan in the first year if sales are drastically lower

- The new owners were planning to increase revenues based on the market research that may fail

- Competition: Nearby new Panera store under construction that will open in April 2027

- “Regular customers” who patronized the previous owner’s bakery may not continue

Family planning meetings: An Opportunity to Teach Financial

Figure 1-2 Grand Opening Date

Bank Loans Check out this link for more info on Bank Loans!

The parents decided that they would inform the family members how they planned to risk all their personal financial resources required by the bank to secure the Corner Bakery operating loans as needed in the future. Bob and Beth agreed that they were willing to risk all their life savings that they accumulated in the twenty-year marriage. They also agreed to risk the home equity since their residence was nearly paid off. The 25-year mortgage had six years remaining. When the Smiths discussed a home equity loan with the bank, the loan officer committed to lending money on the residence contingent on their other financial resources available to secure the new business loan. Bob’s 401-K company retirement savings plan would be available if needed; however, the 401K money would not be drawn on unless absolutely needed after all other money sources were spent since federal income tax penalties would be owed.

Financial Statements Check out this link for more info on Financial Statements!

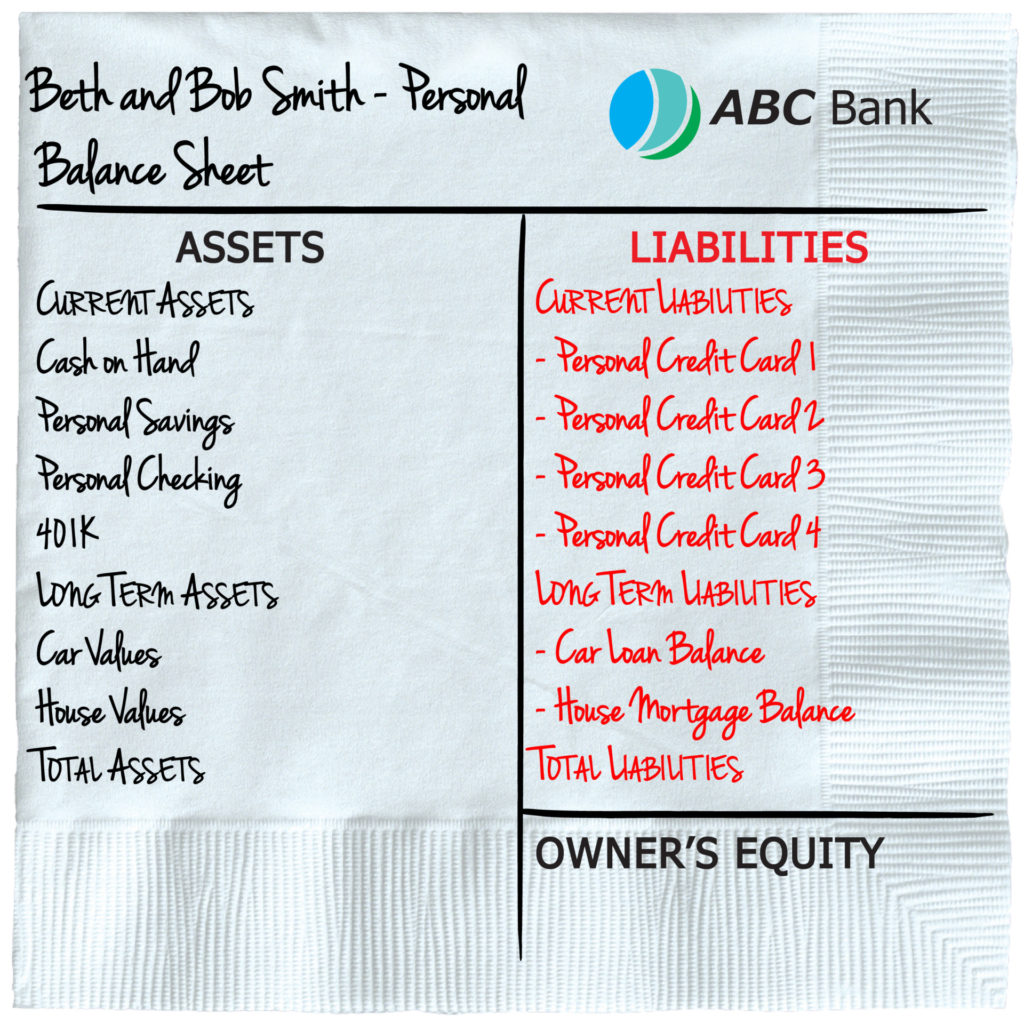

Another source of business financing will be credit cards for business expenses. Beth explained to the children that the banker would require a completed personal financial statement prior to a loan commitment for the bakery operation.

Figure 1-3 Personal Balance Sheet

Mentorship Check out this link for more info on Mentorship!

Since Beth was a dedicated bakery employee during the past seven years, Nancy and her husband, Jim committed to mentoring Beth preparing her for the new ownership effective January 1, 2026. When employed by the Jackson’s, Beth’s responsibilities had been food preparation and serving the customers. The Jacksons wanted to support Beth with all aspects of her new bakery operation. They agreed to offer expertise from their twenty years of business ownership experiences. The owners recommended that Beth devote many hours preparing the Corner Bakery business plan. When Nancy purchased the business, she and her husband did not write out a plan prior to taking ownership. Too many mistakes resulted from the lack of planning were the Jackson’s comments to the new owners. Nancy explained to Beth that to obtain bank financing for the bakery at a future time if needed, a lender will require a minimum of financial records to secure a bank loan. Both parties discussed the merits of a written business plan.

Figure 1-4 Grand Opening Date

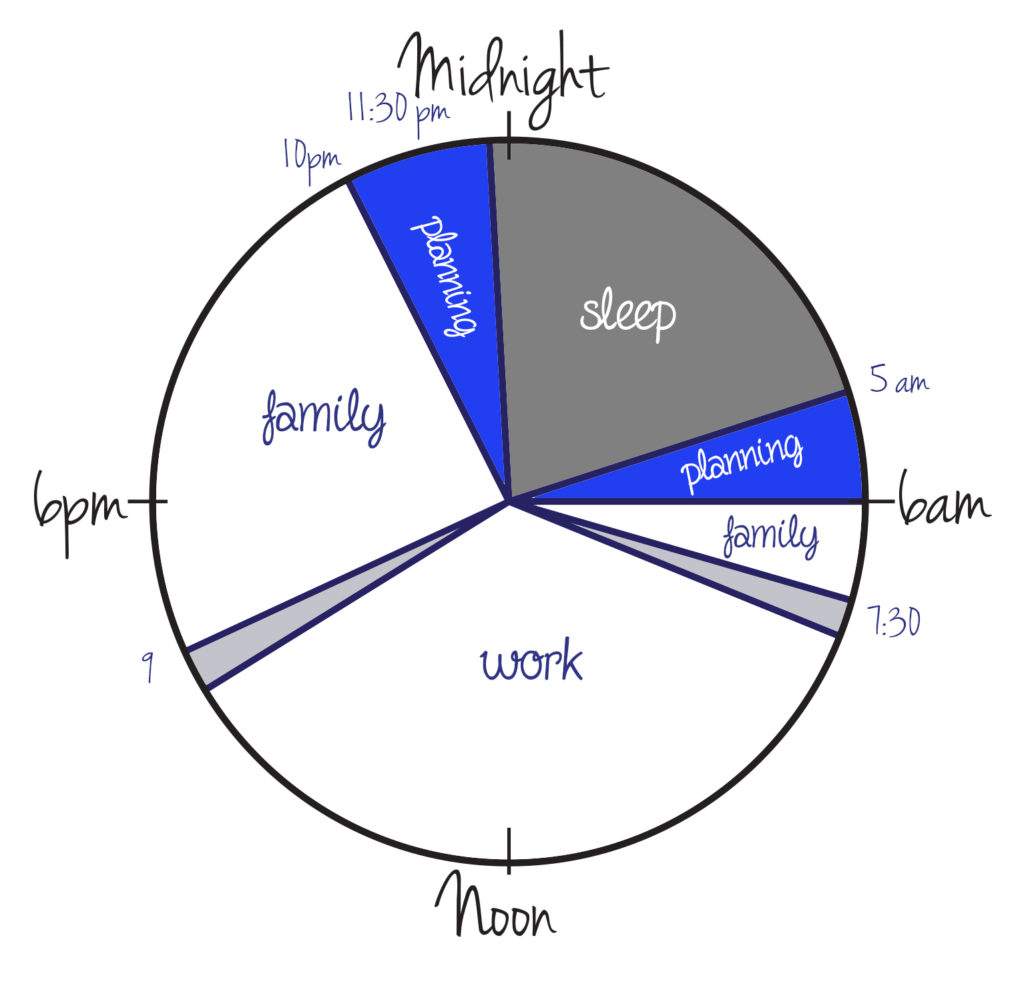

Time management and goal setting

Figure 1-5 Time Management Pie Chart

Beth sets goals for her business:

Time Management Check out this link for more info on Time Management!

Beth makes commitment to herself, her husband and four children to set time aside for planning a successful family business during the months ahead as she prepares for the startup. She studies her 24-hour day and considers her family’s needs as she develops a revised work schedule. Plans were to budget twenty hours per week to devote to planning the business startup.

Case Study: Beth’s allotted time to work on business plan

Case Study: Beth’s allotted time to work on business plan

Goal Setting Check out this link for more info on Goal Setting!

Beth considers herself to be a morning person. Early mornings are best quiet time for internet research and planning, so she decided to begin the day at 5:00 AM. Also, she plans to use hours during the weekend to accomplish her goal. Bob encourages Beth to make these life style changes that will serve as a role model for each family member.

Beginning in August 2025, the five months prior to the Grand Opening Day, Beth and Bob with support of the two college-aged children committed to writing a business plan. The same question was often mentioned by family member. “Where do we start planning for the Grand Opening Day on January 1, 2026?”

Case Study: Beth begins financial planning

Figure 1-6 Grand Opening Date

![]() Beth called their banker at ABC Bank who provided the loans for the Smith’s when they purchased a new sedan two years ago and the home mortgage in a previous year. They assumed that since their loans were in good standing, the bank will make the business loans. In the interview to discuss a future business-operating loan she became uncomfortable discussing the bakery financing with the bank personnel. It seemed to Beth that the banker didn’t understand the future borrowing requirements for the bakery’s day-to-day cash requirements.

Beth called their banker at ABC Bank who provided the loans for the Smith’s when they purchased a new sedan two years ago and the home mortgage in a previous year. They assumed that since their loans were in good standing, the bank will make the business loans. In the interview to discuss a future business-operating loan she became uncomfortable discussing the bakery financing with the bank personnel. It seemed to Beth that the banker didn’t understand the future borrowing requirements for the bakery’s day-to-day cash requirements.

![]() After a disappointing interview with ABC Bank, Beth called the XYZ Bank to set an interview with the bank’s small business officer to begin making financial planning to secure the bakery operating capital. The banker explained that short term and long financial loan commitments should be set up prior opening the new business. During the meeting, the bank personnel provided a personal balance sheet to be completed by the Smiths’ and returned for the loan committee’s approval.

After a disappointing interview with ABC Bank, Beth called the XYZ Bank to set an interview with the bank’s small business officer to begin making financial planning to secure the bakery operating capital. The banker explained that short term and long financial loan commitments should be set up prior opening the new business. During the meeting, the bank personnel provided a personal balance sheet to be completed by the Smiths’ and returned for the loan committee’s approval.

Simple personal balance sheet drawing:

Figure 1-7 Personal Balance Sheet

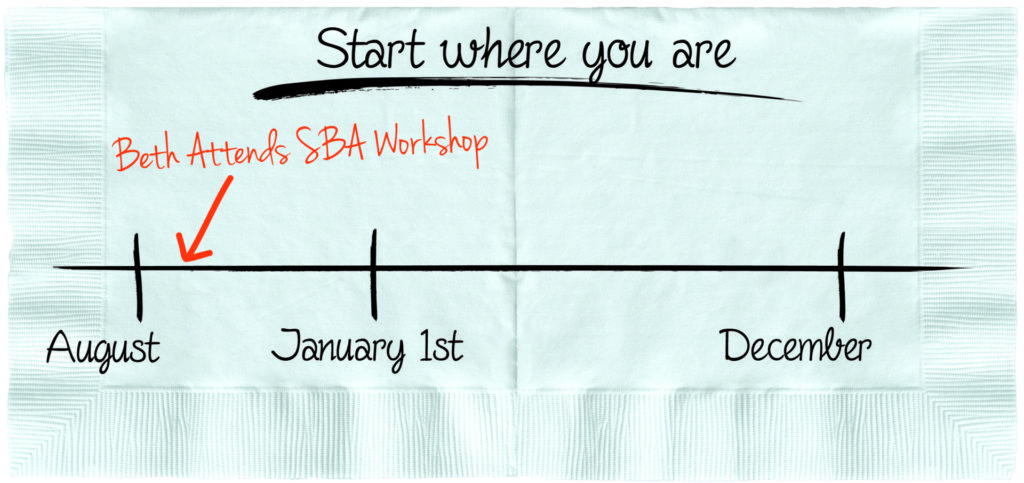

Case Study: Beth attends SBA Workshop

Figure 1-8 Beth Attends Workshop Date

The US Small Business Administration (SBA)

Click here for more information on the US Small Business Administration website!

`

They're an invaluable resource that we'll be using throughout this course. You'll find tons of useful entrepreneurial information.

The local paper announced a free Small Business Administration (SBA) Workshop that would cater to individuals who were considering a small business start-up. To Beth’s surprise neighbors and friends were also attending. Guest speakers included an Attorney, Certified Public Accountant (CPA), Insurance Broker, Bank Loan officer, SBA personnel, and respected entrepreneurs who informed the attendees. The full day workshop was sponsored by a local bank that solicits operating loans for business owners.

SBA personnel introduced the www.sba.gov free resources. The most attention was devoted to writing the business plan. At the end of the full of day, Beth had a feeling of being overwhelmed but was excited to share the experience with the family during the dinner hour.

Each speaker emphasized the need for those in the process of writing a business plan.

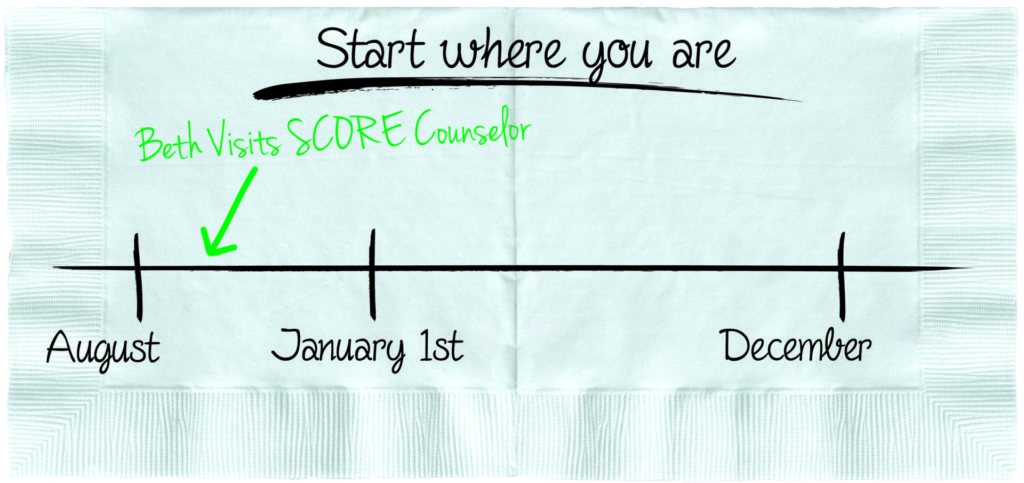

Case Study: Beth visits SCORE Counselor

Figure 1-9 Beth Visits SCORE Counselor

SCORE (Service Corps of Retired Executives)

Click here for more information on the Service Corps of Retired Executives!

`

They're another invaluable resource that we'll be using throughout this course. You'll find tons of useful entrepreneurial information.

Mary, a business owner friend recommended that Beth visit the local at the Service Corps of Retired Executives (SCORE) personnel at the Chamber of Commerce office. Two years prior Beth’s friend, Mary started a retail shop. The SCORE Counselor had made several introductions to free websites resources including a business plan outline that was helpful in the beginning, so Mary encouraged Beth to make the appointment. The counselor introduced Beth to two business plan outlines.

During the interview at the Chamber office Beth informed the counselor that she was in the process of applying for a business operating loan at the XYZ Bank. The purpose of her visit was to get acquainted with the resources available in the startup phase. Beth explained that she had no previous business ownership experience. While attempting her first SCORE meeting, the staff informed Beth of additional web-based resources that she needed to gather data as she researches her business.

Case Study: A ‘teachable’ opportunity for Dad – Dad’s creativity

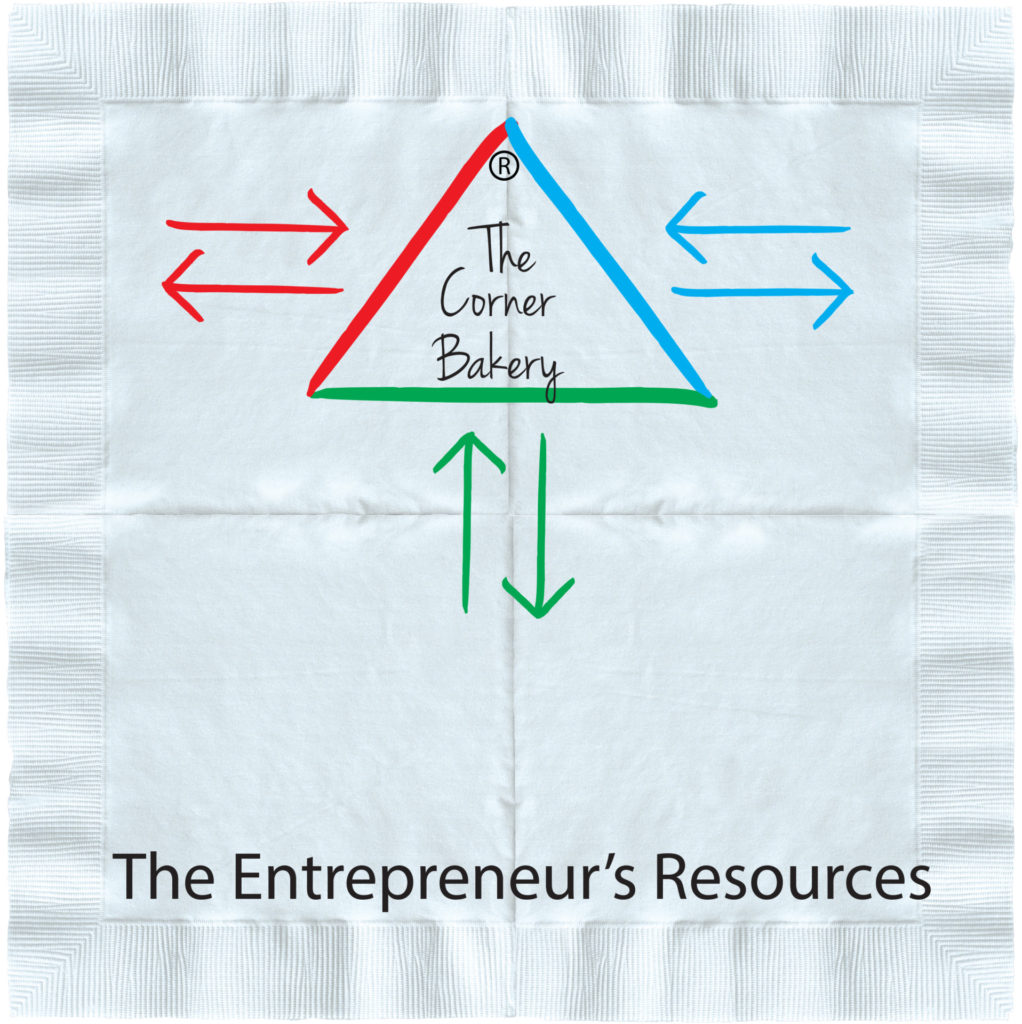

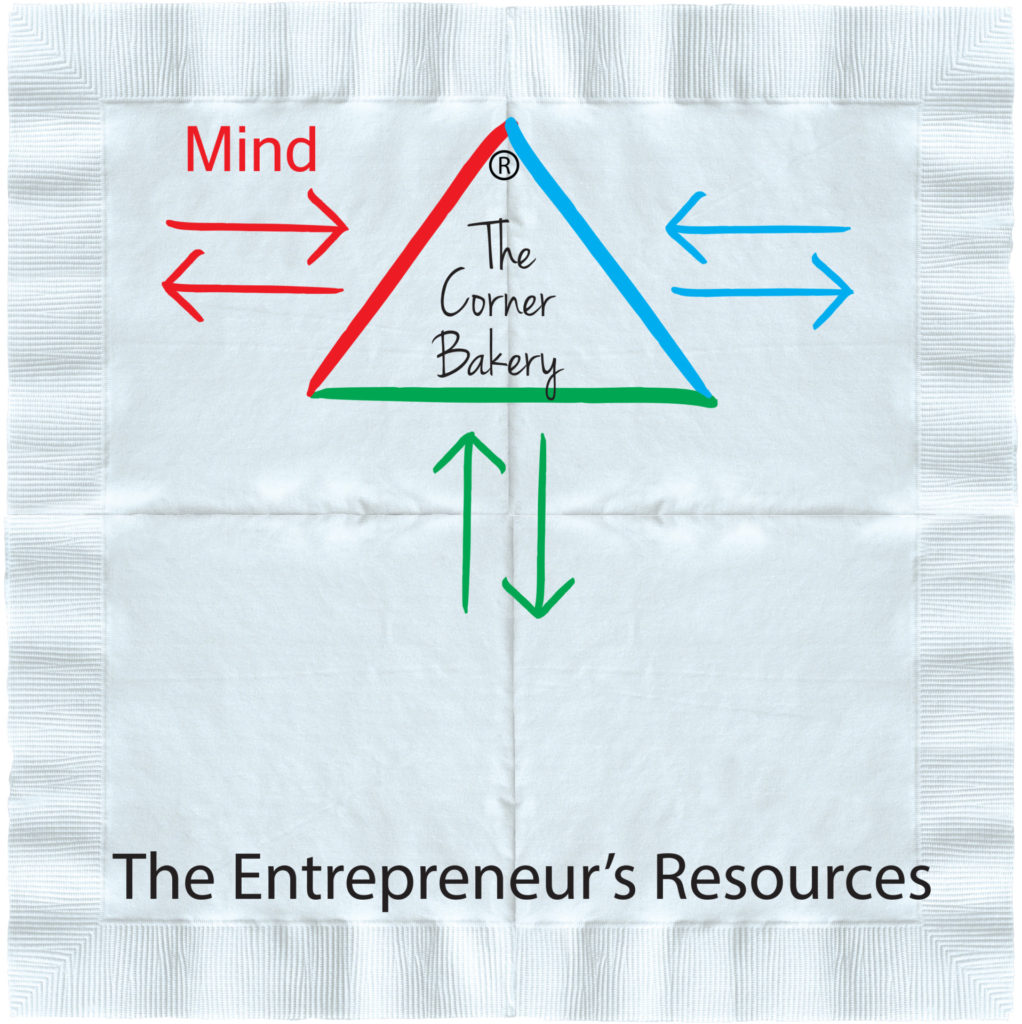

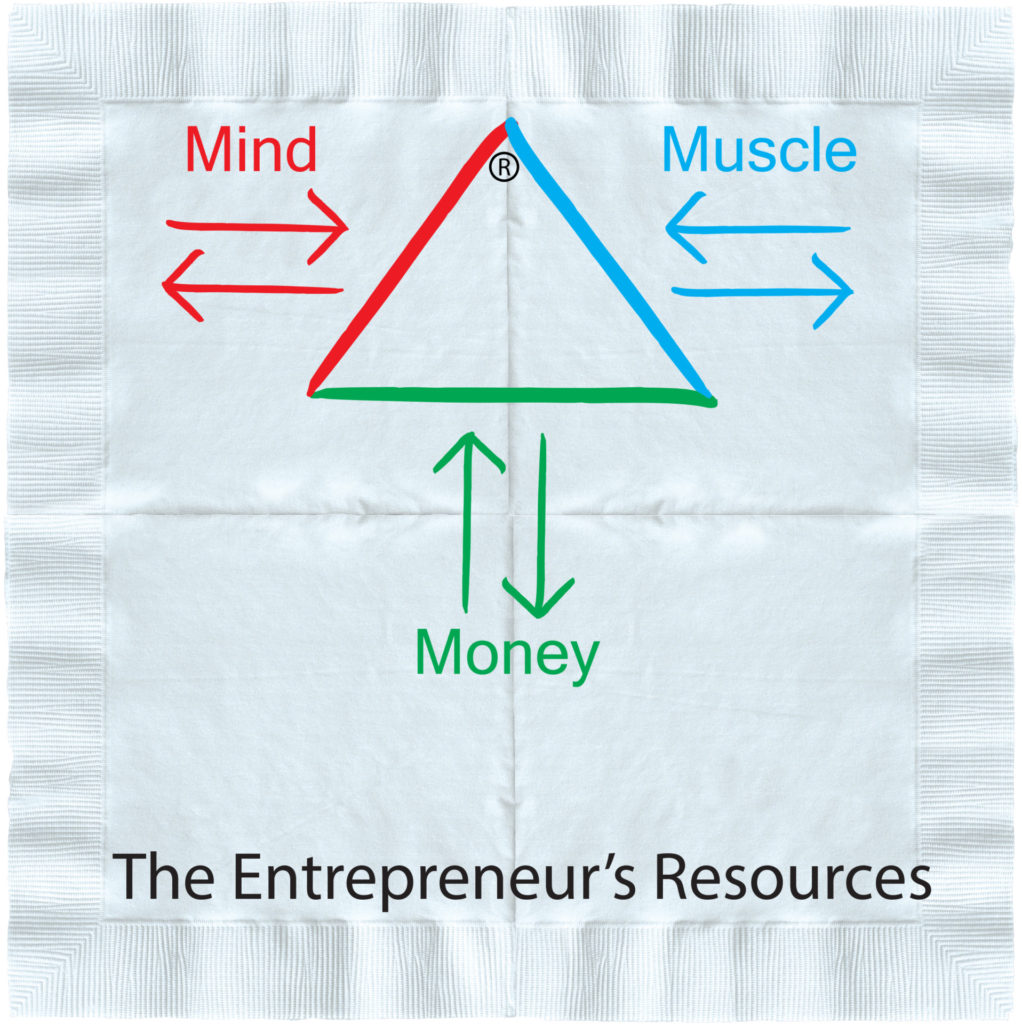

Figure 1-10 The Entrepreneur’s Resource Triangle

After a few weeks of family planning meetings, Dad saw an opportunity to teach the children about MIND resources available to them as they developed the bakery business plan.

Mind Resources:

The Human Mind Check out this link for more info on the human mind!

- Banker

- Attorney

- Certified Public Accountant (CPA)

- Personal friends who are entrepreneurs

- Nancy – Beth’s previous employer

- SCORE Association

- Chamber of Commerce

- Small Business Development Center (SBDC)

- Small Business Administration (SBA)

Dad’s Creativity: Dad begins to draw a triangle on a dinner napkin…

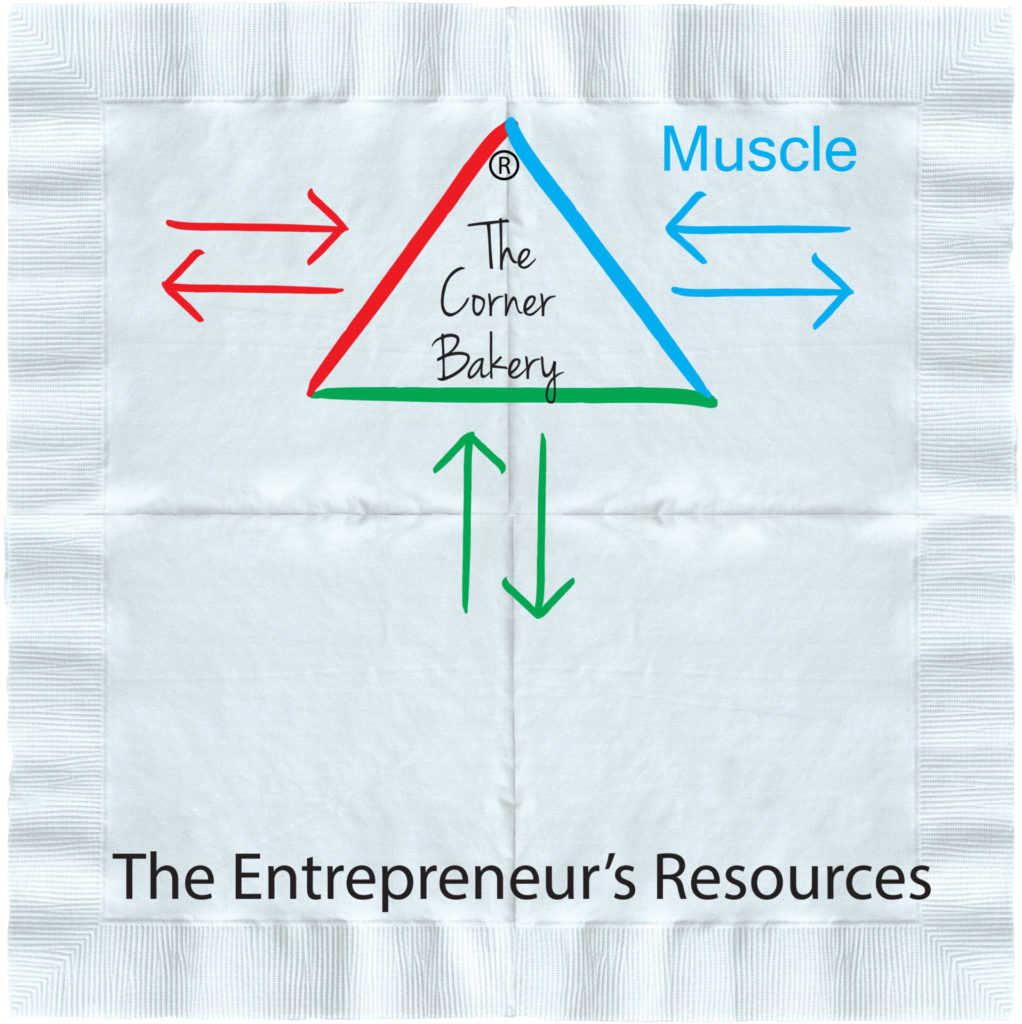

Figure 1-11 The Entrepreneur’s Resource Triangle

After a few weeks of family planning meetings, Dad saw an opportunity to teach the children about MUSCLE resources available to them as they developed the bakery business plan.

Muscle Resources:

- Teenage children

- Mom – Daily Management

- Dad – Oversight and Management

Dad’s Creativity: Dad begins to draw a triangle on a dinner napkin…

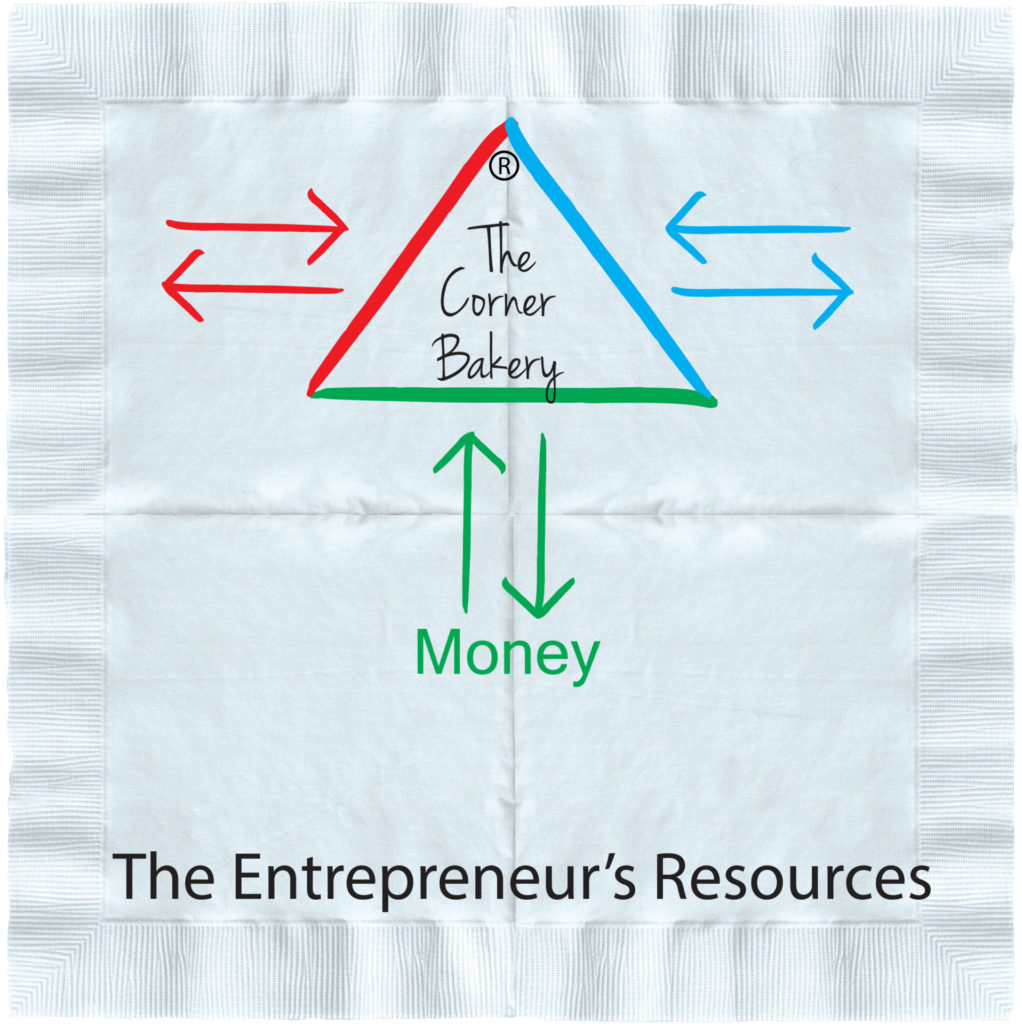

Figure 1-12 The Entrepreneur’s Resource Triangle

After a few weeks of family planning meetings, Dad saw an opportunity to teach the children about MONEY resources available to them as they developed the bakery business plan.

Money Resources:

- Bank – personal savings

- 401(k) – Bob’s company retirement fund

- Home equity loan

- Credit cards

- Beth’s parents co-sign loan

Dad’s creativity: Dad begins to draw a triangle on a dinner napkin…

Figure 1-13 The Entrepreneur’s Resource Triangle

Concept: The Entrepreneur’s Resources

Concept: The Entrepreneur’s Resources

Question: Where does an entrepreneur start planning in the startup?

Answer: Starting at square one.

The small business owner inventories their resources needed to successfully compete in a very competitive business environment. What are Smith family resources? As a risky family business venture, they have “mind,” “muscle,” and “money” resources that will contribute to a successful bakery.

Let’s group the resources as follows:

Mind

- Beth’s part time experience working in the Corner Bakery

- Husband’s support and accounting experience

- Children’s computer skills researching the internet

- SCORE Counselor offering advice

- Banker assisting with financial advice

- Previous owners mentoring Beth

Muscle

- Beth’s full-time employment as Corner Bakery manager/owner

- Bob’s part time employment

- Two college aged children

- Two high school children

- Part time employees

Money

- Family savings account

- Personal credit cards

- Home equity loan

- Bob’s 401K retirement account

- Beth’s parents cosigning business loans

Figure 1-14 The Entrepreneur’s Resources Triangle

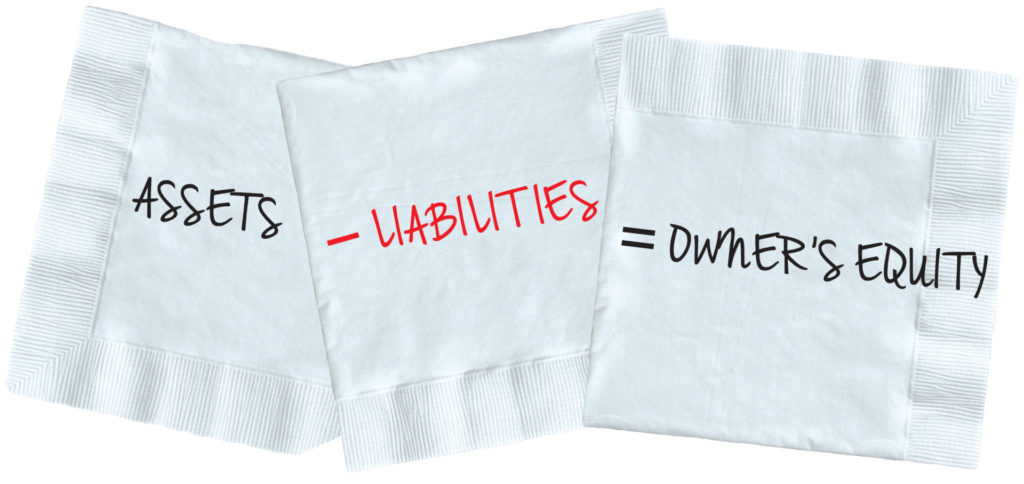

The measurable components of money

Assets

Assets Check out this link for more info on Assets!

Assets are anything that adds value to the owner. They can be converted to cash, and that amount of cash is the value of the asset. Examples are checking account balances, savings account balances, cash on hand, cars, antiques, collectibles, retirement funds, and houses. Assets are usually listed on the personal balance sheet in order of their liquidity. This basically means the ease that they can be converted to cash. Obviously, cash (current assets) would be the easiest, so it would be listed first, and houses, long term credit, collectibles and some retirement funds would be listed lower on the list as they take longer to convert to cash.

Liabilities

Liabilities Check out this link for more info on Liabilities!

Liabilities are debts owed by the owners. They remove cash from the owner’s hand or bank accounts. They are debts, both short term and long term, both secured and unsecured. Examples include balances on credit cards, balances on car loans, balances on mortgage loans, and any taxes or other obligations that are outstanding.

Calculations

Calculations Check out this link for more info on the Basic Accounting Equation!

With these two categories of looking at your money, some calculations can be made to give some other data. The easiest, and most powerful, is Owner’s Equity. Simply put, Assets minus Liabilities equals Owner’s Equity. In fact, that is the basic accounting equation that will be covered next.

Case Study: The Basic Accounting Equation

The formula for the basic accounting equation is assets minus liabilities equals’ owner equity.

Figure 1-15 Basic Accounting Equation

As a simple reminder, when the business owner enters an accounting transaction on one side of the equation she must enter an offsetting entry in the opposite side of the accounting equation, also keeping the financial statement in balance as follows:

5 – 3 = 2

or

5 – 3 (+3) = 2 (+3) ==> 5 = 2 + 3

Assets – Liabilities = Owner’s Equity

Assets = Owner’s Equity + Liabilities

Assets – Owner’s Equity = Liabilities

Owner’s Equity = Assets – Liabilities

Liabilities = Assets – Owner’s Equity

Assets = Owner’s Equity – Liabilities

To introduce the balance sheet: assets, liabilities and owner’s equity.

Equity Check out this link for more info on Equity!

In financial accounting the balance sheet is a summary of financial balances. As seen the basic accounting equation is an algebraic equation (assets minus liabilities equals owner equity). Another way to look at the equation is that assets = liabilities + owner’s equity. This method shows that assets were financed either by borrowing money (debt) or using the Corner Bakery owners’ cash (owner’s equity) to start a new business venture.

Figure 1-16 Personal Balance Sheet

The balance sheet statement is called a ‘snapshot’ of the owners’ “money resources” as of a specific date, for example, January 1. More frequent financial statements may be requested by the lender when a business owner applies for additional working capital to pay expenses during the year.